How diversified are your investments?

2 min video about the lack of diversification in stock market indexes and cryptos

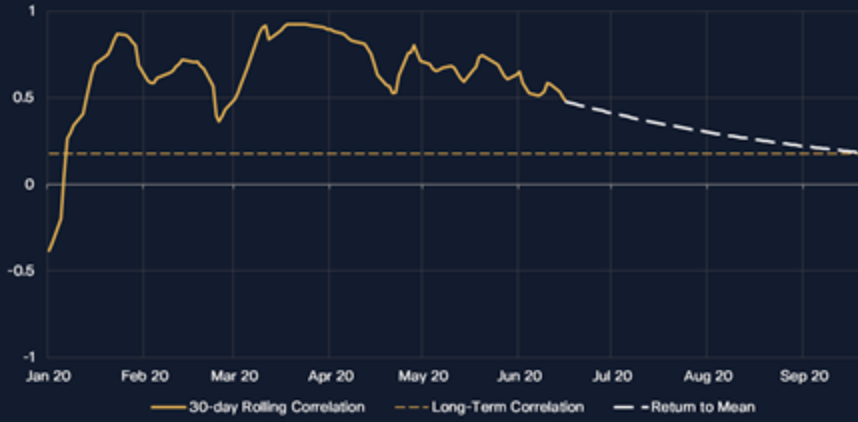

It is often touted that BTC is a good way to diversify your portfolio as being over 11 years since it started trading, BTC has almost zero correlation with equities if you were to compare it with the S&P500. However, BTC price fell considerably in March 2020, as did the S&P500, but since then this asset has outperformed the S&P500 as its correlation returns to norm i.e. zero. Will we see other quoted companies follow MicroStrategy which has recently bought BTC since...

2 min video about the lack of diversification in stock market indexes and cryptos

It is often touted that BTC is a good way to diversify your portfolio as being over 11 years since it started trading, BTC has almost zero correlation with equities if you were to compare it with the S&P500. However, BTC price fell considerably in March 2020, as did the S&P500, but since then this asset has outperformed the S&P500 as its correlation returns to norm i.e. zero. Will we see other quoted companies follow MicroStrategy which has recently bought BTC since...